Buying your first home is exciting, but it also requires careful financial planning. Many first-time buyers focus only on the home price and forget about other important costs.

Learning the right budgeting tips for first-time homebuyers helps you avoid financial stress and prepare for homeownership with confidence.

This guide explains how to plan your budget before buying a home.

Why Budgeting Is Important Before Buying a Home

Creating a budget helps you understand how much home you can realistically afford.

A clear homebuying budget helps you:

- Avoid taking on too much debt

- Prepare for upfront costs

- Plan monthly mortgage payments

- Maintain financial stability after moving in

Good budgeting ensures your home purchase fits your long-term financial goals.

Budgeting Tips for First-Time Homebuyers

Understand Your Monthly Income

The first step in budgeting is knowing your total monthly income after taxes.

Include all reliable income sources such as:

- Salary or wages

- Bonuses or commissions

- Business income

- Side income if stable

Once you know your income, you can determine how much you can safely spend on housing.

Follow the 28% Housing Rule

Many financial experts recommend the 28% rule for housing expenses.

This means your monthly housing costs should not exceed 28% of your gross monthly income.

Housing costs include:

- Mortgage payment

- Property taxes

- Home insurance

- HOA fees (if applicable)

This rule helps keep your mortgage affordable.

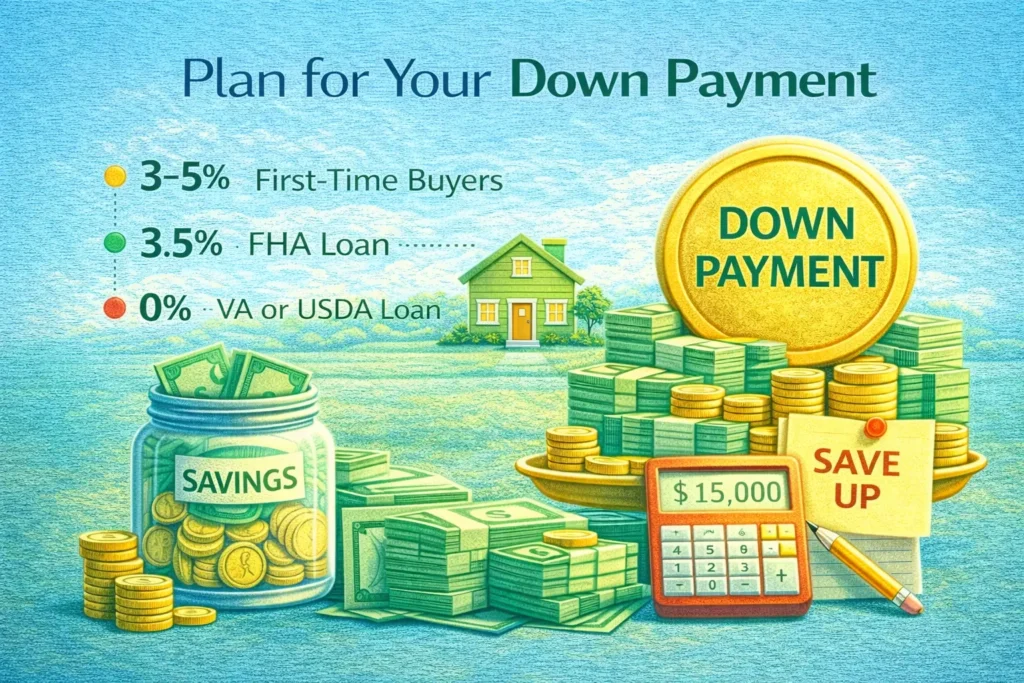

Plan for Your Down Payment

The down payment is one of the biggest upfront costs when buying a home.

Typical down payments include:

- 3–5% for many first-time homebuyer programs

- 3.5% for FHA loans

- 0% for certain VA or USDA loans

Saving more for a down payment can reduce your monthly mortgage payment.

Prepare for Closing Costs

Many first-time buyers forget about closing costs.

Closing costs usually range between 2% and 5% of the home price.

These costs may include:

- Loan origination fees

- Appraisal fees

- Title insurance

- Legal and administrative fees

Planning ahead prevents surprises at closing.

Build an Emergency Fund

After buying a home, unexpected expenses can happen.

For example:

- Home repairs

- Appliance replacement

- Maintenance costs

Experts recommend saving 3–6 months of living expenses as an emergency fund.

This protects your finances after purchasing a home.

Reduce Debt Before Applying for a Mortgage

Your debt-to-income ratio (DTI) plays a big role in mortgage approval.

To improve your chances of approval:

- Pay down credit card balances

- Avoid new loans before applying

- Reduce monthly debt payments

Lower debt makes it easier to qualify for better mortgage terms.

Planning to buy your first home?

Our specialists help first-time buyers understand their budget and find the right home loan.

Track Your Monthly Spending

Tracking your spending helps identify where your money goes each month.

Simple budgeting tools include:

- Banking apps

- Budget spreadsheets

- Personal finance apps

Cutting unnecessary expenses can help you save faster for your home purchase.

Work With a Mortgage Expert

First-time buyers often benefit from professional guidance.

A mortgage expert can help you:

- Understand loan options

- Estimate monthly payments

- Calculate how much home you can afford

- Get pre-approved for a mortgage

Professional advice can make the homebuying process easier.

Ready to Buy Your First Home?

At JL Lending we help first-time homebuyers find affordable loan options and start their homeownership journey.

Read More How Mortgage Interest Rates Affect Your Monthly Payment

FAQs

How much should first-time homebuyers budget for a house?

Most experts recommend keeping housing costs below 28% of your monthly income to maintain a healthy budget.

What is the biggest cost when buying a home?

The largest upfront costs usually include the down payment and closing costs.

How much savings should I have before buying a home?

You should have savings for:

- Down payment

- Closing costs

- Emergency fund

- Moving expenses