Most lenders prefer a credit score of at least 620 for a bank statement loan, but stronger scores can help you qualify for better rates, lower down payments, and more flexible loan terms.

What Is a Bank Statement Loan?

A bank statement loan is a non-QM mortgage designed for borrowers who may not qualify using traditional tax returns.

Instead of W-2s or tax documents, lenders review:

- Personal bank statements

- Business bank statements

- Deposit history

- Cash flow consistency

These loans are commonly used by:

- Self-employed borrowers

- Business owners

- Freelancers

- Independent contractors

Minimum Credit Score for a Bank Statement Loan

Most lenders typically require:

- 620+ minimum credit score

However, requirements vary depending on:

- Down payment

- Loan amount

- Cash reserves

- Property type

- Overall financial profile

How Credit Score Affects Your Loan

Your credit score can impact:

- Loan approval

- Interest rates

- Down payment requirements

- Loan terms

General Rule:

- Higher score → better loan terms

- Lower score → higher lender risk

Want to understand what loan options you may qualify for?

✔ Review Flexible Mortgage Programs

✔ Explore Bank Statement Loan Options

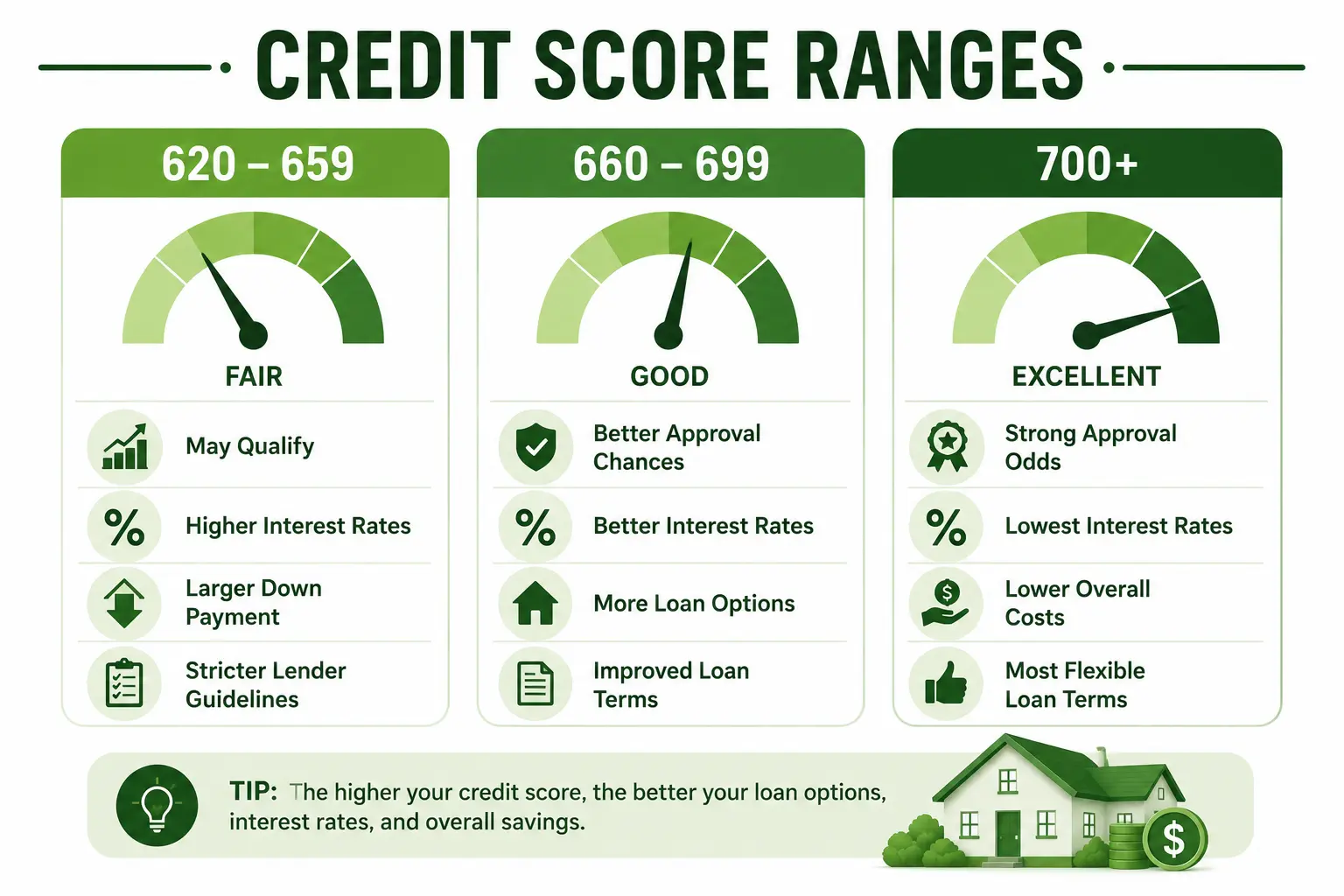

Credit Score Ranges Explained

620–659 Credit Score

Borrowers in this range may still qualify, but could see:

- Higher interest rates

- Larger down payment requirements

- Stricter lender guidelines

660–699 Credit Score

This range may provide:

- Better approval chances

- More lender options

- Improved mortgage terms

700+ Credit Score

Borrowers with strong credit often receive:

- Better interest rates

- Lower financing costs

- More flexible approval options

Can You Get a Bank Statement Loan With Bad Credit?

Yes, some lenders work with lower-credit borrowers.

However, you may need:

- Larger down payment

- Higher cash reserves

- Strong bank deposits

- Lower debt levels

What Else Do Lenders Look At?

Credit score is important, but lenders also review:

- Monthly bank deposits

- Income consistency

- Business cash flow

- Debt-to-income ratio

- Property type

Strong overall finances can help offset a lower credit score.

How to Improve Your Chances of Approval

1. Increase Your Credit Score

Pay down balances and avoid missed payments before applying.

2. Reduce Existing Debt

Lower debt obligations improve your borrower profile.

3. Maintain Strong Bank Deposits

Consistent deposits help verify income stability.

4. Save for a Larger Down Payment

More equity can reduce lender risk.

Example Scenario

Borrower A

- 720 credit score

- Strong deposits

- 20% down payment

Better rates and approval flexibility likely

Borrower B

- 620 credit score

- Higher debt

- Limited reserves

Approval may still be possible with stricter terms

Self-Employed and Exploring Mortgage Options?

Bank statement loans can help borrowers qualify using deposits instead of traditional tax return income.

✔ Compare Your Financing Options

✔ Speak With a Mortgage Specialist

Read More Can You Buy an Investment Property With a Bank Statement Loan in 2026?

FAQs

What credit score is needed for a bank statement loan?

Most lenders prefer at least a 620 credit score, although stronger scores improve loan terms.

Can I get a bank statement loan with bad credit?

Yes, some lenders allow lower scores depending on your overall financial profile.

Does a higher credit score lower interest rates?

Yes. Higher scores often qualify for better rates and lower borrowing costs.

Are bank statement loans easier for self-employed borrowers?

Yes. These loans are designed for borrowers with non-traditional income documentation.

Do bank statement loans require tax returns?

In many cases, no. Lenders usually review bank deposits instead.