When you apply for a mortgage, lenders look closely at your Debt-to-Income Ratio (DTI).

This number helps lenders understand if you can comfortably afford a monthly mortgage payment.

A high DTI may make loan approval harder, while a lower DTI shows lenders that you manage debt responsibly.

This guide explains Debt-to-Income Ratio, how lenders calculate it, and why it matters when buying a home.

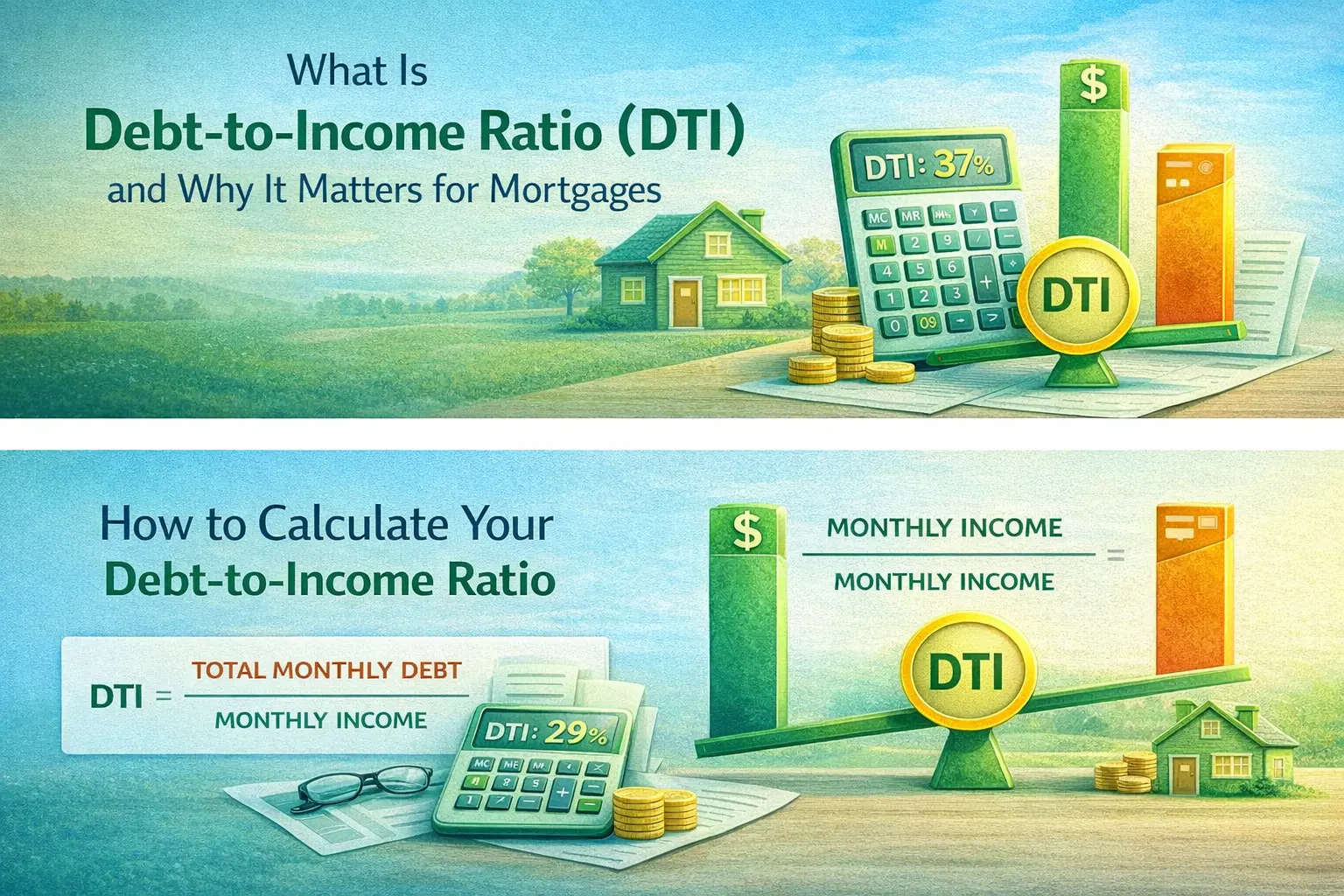

What Is Debt-to-Income Ratio (DTI)?

Debt-to-Income Ratio (DTI) is the percentage of your monthly income that goes toward paying debts.

Lenders use this number to measure your ability to manage monthly payments.

Example

Monthly income: $6,000

Monthly debts:

- Car loan: $400

- Credit cards: $200

- Student loan: $300

Total monthly debt: $900

DTI calculation:

$900 ÷ $6,000 = 15% DTI

This means 15% of your income goes toward debt payments.

Why Debt-to-Income Ratio Matters for Mortgages

Lenders want to ensure borrowers can handle mortgage payments without financial stress.

Your Debt-to-Income Ratio helps lenders determine:

- Whether you qualify for a mortgage

- How much you can borrow

- What loan programs you qualify for

A lower DTI generally improves your chances of loan approval and better interest rates.

Want to know how much home you can afford? Our specialists can review your finances and help you explore the best loan options.

What Is a Good Debt-to-Income Ratio for a Mortgage?

Different loan programs allow different DTI limits.

Typical DTI ranges

- 36% or lower – Excellent for most mortgages

- 37% – 43% – Acceptable for many loan programs

- Above 43% – May be harder to qualify

Some government programs allow slightly higher DTI ratios if other factors are strong.

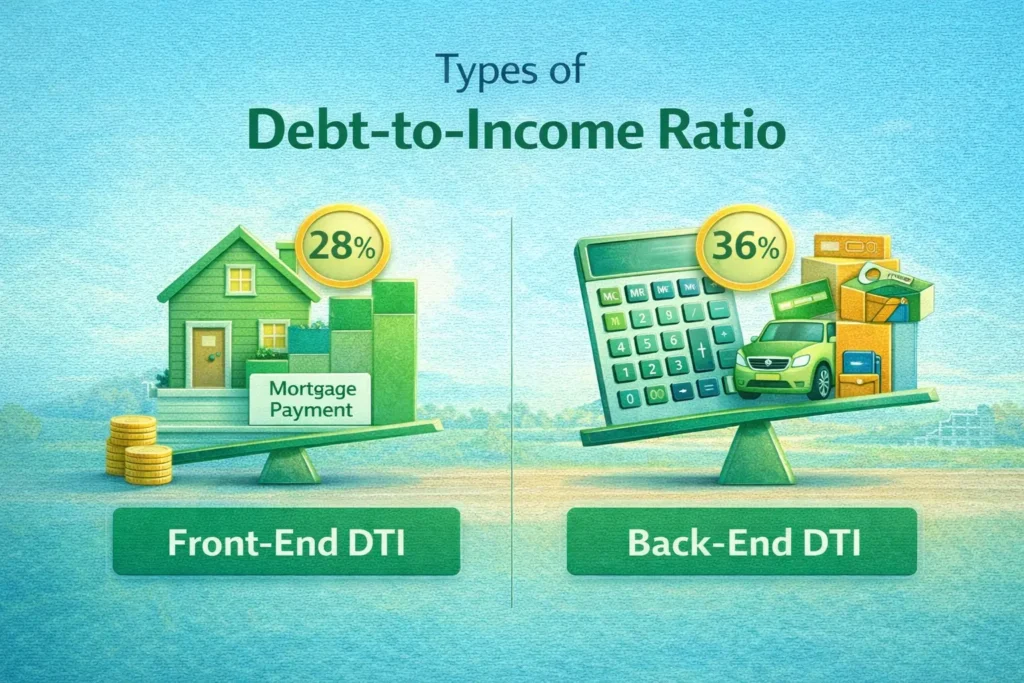

Two Types of Debt-to-Income Ratio

Lenders usually calculate two types of DTI when reviewing a mortgage application.

1. Front-End DTI

This measures housing costs only.

Includes:

- Mortgage payment

- Property taxes

- Homeowners insurance

- HOA fees (if applicable)

2. Back-End DTI

This measures all monthly debts combined.

Includes:

- Housing expenses

- Credit cards

- Car loans

- Student loans

- Personal loans

Most lenders focus more on back-end DTI.

How to Calculate Your Debt-to-Income Ratio

You can estimate your Debt-to-Income Ratio using a simple formula.

Step-by-step

- Add all monthly debt payments

- Calculate your gross monthly income

- Divide debts by income

- Multiply by 100

Example:

Total monthly debt: $1,200

Monthly income: $5,000

DTI calculation:

$1,200 ÷ $5,000 = 24% DTI

How to Lower Your Debt-to-Income Ratio

A lower Debt-to-Income Ratio can improve your chances of mortgage approval.

Simple ways to reduce your DTI include:

- Pay down credit card balances

- Avoid taking new loans before applying

- Increase your income if possible

- Pay off smaller debts first

- Consider a larger down payment

Even small changes can make your DTI more attractive to lenders.

Need help improving your mortgage approval chances? Our experts can guide you on lowering your DTI and qualifying faster.

How Mortgage Experts Can Help

Understanding your Debt-to-Income Ratio before applying for a mortgage can save time and prevent loan delays.

Mortgage brokers can help you:

- Calculate your DTI accurately

- Review your financial profile

- Compare mortgage programs

- Identify ways to qualify faster

Not sure if your Debt-to-Income Ratio qualifies for a mortgage? Our experts can review your finances and help you explore the best loan options.

Conclusion

Your Debt-to-Income Ratio plays a major role in mortgage approval.

Keeping your DTI low shows lenders that you can manage debt responsibly and handle a new mortgage payment.

Before applying for a home loan, it is helpful to calculate your DTI and review your financial situation carefully.

Read More What Is Private Mortgage Insurance (PMI) and How to Remove It?

FAQs

What is a good Debt-to-Income Ratio for a mortgage?

Most lenders prefer a DTI below 36%, but some loan programs allow up to 43% or higher.

Can I get a mortgage with a high DTI?

Yes. Some loan programs may allow higher DTI ratios, especially if you have strong credit or a large down payment.

Does credit card debt affect Debt-to-Income Ratio?

Yes. Minimum credit card payments count toward your monthly debt obligations.

Does rent count in Debt-to-Income Ratio?

Rent may count as a housing expense when lenders evaluate your financial profile.

How can I improve my Debt-to-Income Ratio quickly?

You can improve your DTI by paying off small debts, reducing credit card balances, or increasing your income.