DSCR loans are usually denied due to low rental income, poor credit, high risk properties, or incomplete documentation.

DSCR loans are popular because they focus on rental income instead of personal income. But even with flexible guidelines, not every application gets approved.

What Is a DSCR Loan?

A DSCR (Debt-Service Coverage Ratio) loan is based on a property’s ability to generate income.

Lenders evaluate:

- Rental income

- Monthly loan payments

- Property cash flow

If income doesn’t cover the debt, approval becomes difficult.

Top Reasons DSCR Loans Get Denied

1. Low DSCR Ratio

This is the most common reason.

- DSCR below 1.0 means income is not enough

- Many lenders prefer 1.2 or higher

Low cash flow = higher risk

2. Poor Credit Score

Even though income is property-based, credit still matters.

- Low credit score reduces approval chances

- Higher risk = stricter conditions or denial

3. Insufficient Down Payment

Most DSCR loans require:

- 20%–25% down payment

Lower down payment can lead to rejection

4. Unstable or Low Rental Income

If the property cannot generate consistent income:

- Loan may be denied

- Short-term rental income may be scrutinized

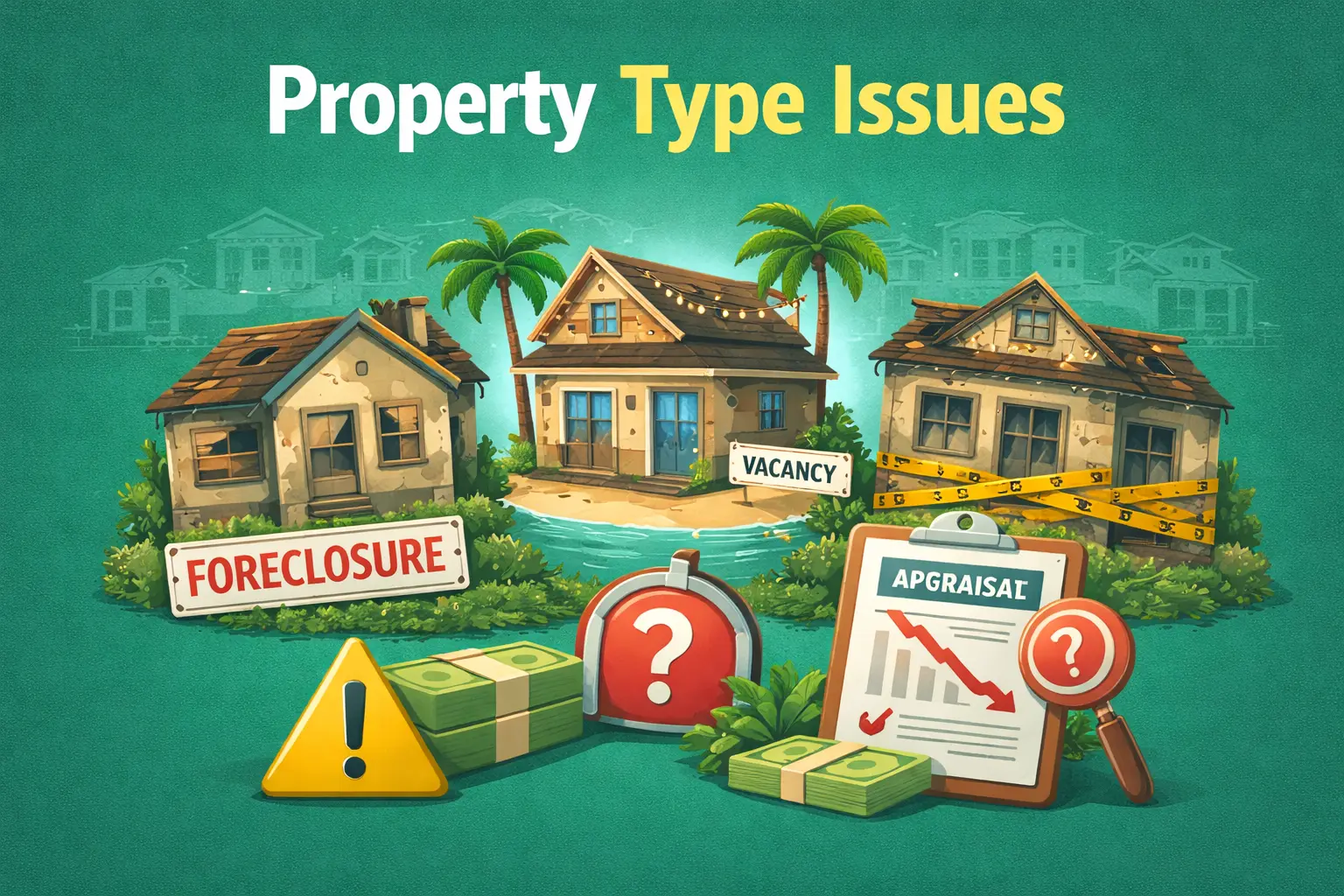

5. Property Type Issues

Some properties are considered high-risk:

- Unique or hard-to-sell homes

- Properties in low-demand areas

- Condition or appraisal issues

6. High Debt-to-Income (DTI)

Even though DSCR focuses on property income:

- Lenders may still review your overall debt

- High DTI increases risk

7. Incomplete or Incorrect Documentation

Missing documents can delay or deny approval.

Common issues:

- Incomplete bank statements

- Missing lease agreements

- Errors in application

Worried about getting denied?

✔ Check Your DSCR Loan Eligibility

✔ Get Expert Guidance Before Applying

8. Appraisal Comes in Low

If the property value is lower than expected:

- Loan amount may be reduced

- Application may be denied

9. Market Risk Factors

Lenders consider:

- Local market conditions

- Rental demand

- Property liquidity

Weak markets = higher risk

How to Avoid DSCR Loan Denial

You can improve your chances by:

- Choosing properties with strong rental income

- Improving your credit score

- Preparing full documentation in advance

- Putting down a larger down payment

- Working with an experienced lender

Ready to Get Approved for a DSCR Loan?

Avoid common mistakes and improve your chances of success.

✔ Apply for a DSCR Loan Today

✔ Speak With an Investment Loan Expert

Read More Pros and Cons of DSCR Loans

FAQs

What is the most common reason DSCR loans get denied?

Low DSCR ratio (insufficient rental income) is the most common reason.

What DSCR score is required?

Most lenders prefer a DSCR of 1.2 or higher.

Can bad credit affect DSCR loan approval?

Yes, credit score still plays an important role.

Do DSCR loans require rental income?

Yes, rental income is the primary factor for approval.

Can you get denied after pre-approval?

Yes, if new issues arise during underwriting.