A Home Equity Line of Credit, or HELOC, gives you flexible access to funds by using your home’s available equity. Many homeowners choose a HELOC when they want a revolving credit line for improvements, debt management, or major expenses. When you understand how a HELOC works, you can decide whether this option supports your financial goals and long-term plans.

Understanding HELOC

A HELOC allows you to borrow money as needed, similar to a credit card, but secured by your home. It provides a draw period for spending and a repayment phase that follows preset terms. When you understand each part clearly, you can use a HELOC confidently and manage it with long-term financial stability in mind.

How a HELOC Uses Your Home’s Equity

A HELOC calculates your borrowing limit based on the equity you have built in your home. Lenders review your home value and subtract your current mortgage balance to determine your available equity. You gain a larger credit line when your equity grows through payments or appreciation. This structure helps you access funds without selling your property.

How the Credit Line and Draw Period Work

A HELOC includes a draw period that usually lasts five to ten years. During this time, you can borrow funds, repay them, and borrow again as needed. Interest charges apply only to the amount you use from your credit line. After the draw period ends, you enter the repayment phase and begin paying down the entire balance.

HELOC vs Home Equity Loan

| Feature | HELOC | Home Equity Loan |

|---|---|---|

| Loan Type | Revolving credit line | Lump-sum fixed loan |

| Interest Rate | Usually variable | Fixed rate |

| Access to Funds | Borrow as needed during the draw period | Fixed payments for the full term |

| Monthly Payments | Interest-only during the draw period | Fixed payments for full term |

| Best For | Long-term, flexible spending needs | One-time major expenses |

How a HELOC Works From Start to Finish

A HELOC follows a structured timeline that includes borrowing, repayment, and long-term management. You start with a draw period, transition into repayment, and use interest rules that affect your total cost. When you understand each phase clearly, you can use your credit line responsibly and avoid financial stress.

How Borrowing, Repayment, and Interest Charges Work

A HELOC allows you to borrow money during the draw period whenever you need funds. You pay interest only on the amount you use, which helps you manage your budget. After the draw period ends, the loan enters repayment and requires monthly payments that cover principal and interest. This structure supports flexibility during the early phase and clear repayment later.

Variable Rates vs Fixed-Rate HELOC Options

Most HELOCs include variable interest rates that change with market conditions. These rates may rise or fall throughout your loan term. Some lenders also offer fixed-rate HELOC options that lock in stable payments. You choose based on your comfort with market changes and long-term planning.

Minimum Draw Amounts, Withdrawal Rules, and Access Methods

Lenders set rules for how you access funds during the draw period. Some HELOCs require minimum draw amounts, while others allow flexible withdrawals. You can access funds through checks, online transfers, or a dedicated HELOC card. Clear access rules help you plan your spending effectively.

Common Uses for a HELOC

A HELOC supports several financial goals because it offers flexible borrowing. You can use the credit line for planned projects or unexpected expenses. When you use a HELOC strategically, you gain more control over your budget and long-term financial plans.

Home Improvements and Renovations

Many homeowners use a HELOC to finance upgrades or remodels. These improvements increase home value and enhance everyday comfort. You can complete projects without using savings or delaying your plans. A HELOC creates flexibility for long-term property value growth.

Debt Consolidation and Credit Management

A HELOC helps you combine high-interest debt into one manageable payment. You can lower monthly costs and simplify your financial routine. This strategy supports credit improvement when you make consistent payments. You gain more control over debt when you use the funds wisely.

Emergency Funds, Education Costs, and Other Needs

A HELOC gives you access to funds when unexpected expenses arise. You can cover medical bills, tuition, or major household needs. The revolving nature of a HELOC supports planned and unplanned financial situations. This flexibility makes it a valuable tool for long-term financial management.

Pros and Cons of a HELOC

A HELOC gives you flexible access to funds, but it also includes risks that homeowners must understand. Reviewing both sides helps you decide whether a HELOC fits your financial goals and long-term plans.

| Pros | Cons |

|---|---|

| Flexible access to funds during the draw period | Variable interest rates can increase over time |

| Closing costs and annual fees increase the overall cost | Requires discipline to avoid overspending |

| You pay interest only on the funds you use | Uses your home as collateral, increasing risk |

| Can support renovations, debt consolidation, and emergencies | Interest-only payments during the draw period offer short-term relief |

| Potential tax benefits for qualifying improvements | Closing costs and annual fees increase overall cost |

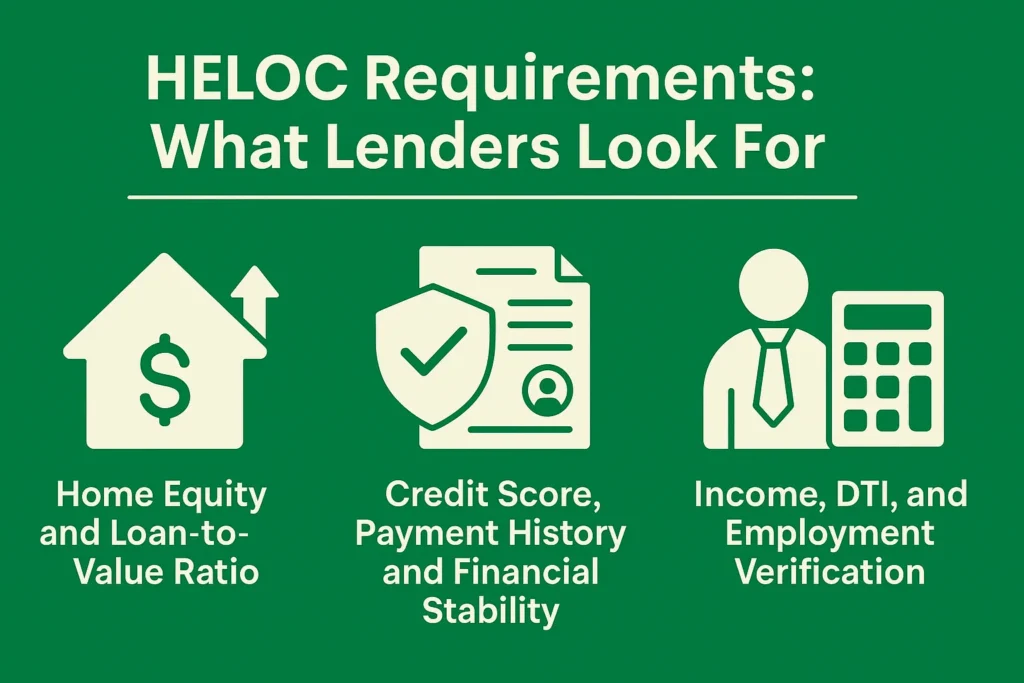

HELOC Requirements: What Lenders Look For

Lenders review several financial factors before approving a HELOC. These requirements ensure that you can manage the credit line responsibly and protect your home’s equity. When you understand these expectations early, you can prepare and improve your approval chances.

Home Equity and Loan-to-Value Ratio

Lenders review your available equity because it determines your borrowing limit. You gain more approval strength when your loan-to-value ratio stays low.

Lenders typically expect:

- At least 15%–20% equity in your home

- A combined loan-to-value ratio below 85%

- A stable property value supported by an appraisal

Credit Score, Payment History, and Financial Stability

Lenders want to see responsible credit use and consistent payment habits. These factors show that you can manage a HELOC responsibly.

Most lenders review:

- Credit scores above 620 for standard programs

- On-time payment history across all accounts

- Stable credit behavior over several months

Income, DTI, and Employment Verification

Your income and debt levels affect your ability to manage future payments. Lenders confirm these details to evaluate repayment strength.

Typical requirements include:

- Debt-to-income ratio below 43%

- Steady employment for at least two years

- Proof of income through pay stubs or tax returns

How to Apply for a HELOC Successfully

You can apply for a HELOC with greater confidence when you understand each step in the process. Lenders review your equity, credit, income, and documents before approving your credit line. Clear preparation helps you move through the application smoothly and secure better terms.

Step 1: Review Your Home Equity and Credit

Start by checking your current mortgage balance and estimating your available equity. You should also review your credit score and payment history. These factors determine your borrowing limit and interest rate. Strong credit and healthy equity help you qualify for a larger line.

Step 2: Compare HELOC Rates and Terms from Multiple Lenders

Lenders offer different rates, fees, and repayment structures. Request estimates so you can compare total costs and draw period rules. You gain valuable insight when you review several offers side by side. This step helps you choose the HELOC that supports your financial goals.

Step 3: Complete the Application and Property Appraisal

Submit your application along with income documents, bank statements, and identification. Lenders then order a property appraisal to confirm your home’s value. You move faster through this stage when your documents stay organized. Clear information helps lenders finalize your credit line.

Step 4: Set Up Withdrawals and Manage Your Line Responsibly

After approval, you receive access to your credit line through checks, transfers, or a HELOC card. You need to track spending and plan withdrawals carefully. Responsible use protects your equity and supports strong financial habits. This approach helps you use your HELOC effectively.

Costs, Rates, and Fees You Should Expect

A HELOC includes several fees that affect your total borrowing cost. You need to understand these expenses before applying because they influence your budget and repayment timeline. Clear cost awareness helps you choose the right HELOC for your goals.

Interest Rates and Margin-Based Pricing

HELOCs usually include variable interest rates that change with market conditions. Lenders add a margin to the index, which determines your final rate. You may also find fixed-rate conversion options for added stability. These rate structures influence your long-term cost.

Annual Fees, Closing Costs, and Withdrawal Fees

Some lenders charge annual fees to keep your credit line open. You may also pay closing costs, including appraisal, title, and document fees. Certain HELOCs include minimum withdrawal fees or early closure charges. These costs vary, so comparing them helps you save money.

How HELOC Costs Affect Your Total Borrowing

Higher rates and additional fees increase your overall cost, especially during heavy use. You reduce costs when you borrow only what you need and repay funds quickly. Smart management helps you maintain financial stability and protect your long-term goals. Understanding these costs improves your decision-making.

Conclusion

A HELOC gives you flexible access to funds by using the equity you built in your home. You can use it for improvements, debt consolidation, or major financial needs while keeping interest costs under control. When you understand the requirements, compare lenders carefully, and manage your credit line responsibly, you can use a HELOC confidently and protect your long-term financial goals. Strong planning helps you borrow wisely and take advantage of the value your home already provides.

FAQs

Most HELOC draw periods last five to ten years, giving you time to borrow as needed. You begin full repayment after the draw period ends and follow the lender’s set timeline.

Many lenders prefer scores above 620 because a HELOC uses your home as collateral. You may qualify with a lower score when you show strong income, low debt, and consistent payment history.

Yes, many homeowners use a HELOC to combine high-interest debt into one manageable payment. This approach helps you lower monthly costs when you use the funds responsibly.

Some lenders charge closing costs, annual fees, or transaction fees. You save money when you compare estimates early and choose a HELOC with competitive pricing and clear terms.