A Loan Estimate is a document your lender provides after you apply for a mortgage. It shows the loan terms, interest rate, monthly payment, and closing costs.

A Loan Estimate helps you understand and compare mortgage offers before committing to a loan.

When Do You Get a Loan Estimate?

Lenders are required to provide a Loan Estimate within 3 business days of your application.

You receive it after:

- Submitting your mortgage application

- Providing basic financial information

- Authorizing a credit check

Why Is the Loan Estimate Important?

The Loan Estimate helps you:

- Compare offers from different lenders

- Understand total loan costs

- Avoid hidden fees

- Make informed decisions

It’s one of the most important documents in the homebuying process.

Want help reviewing your Loan Estimate?

✔ Speak With a Mortgage Expert Today

✔ Compare Loan Offers With Confidence

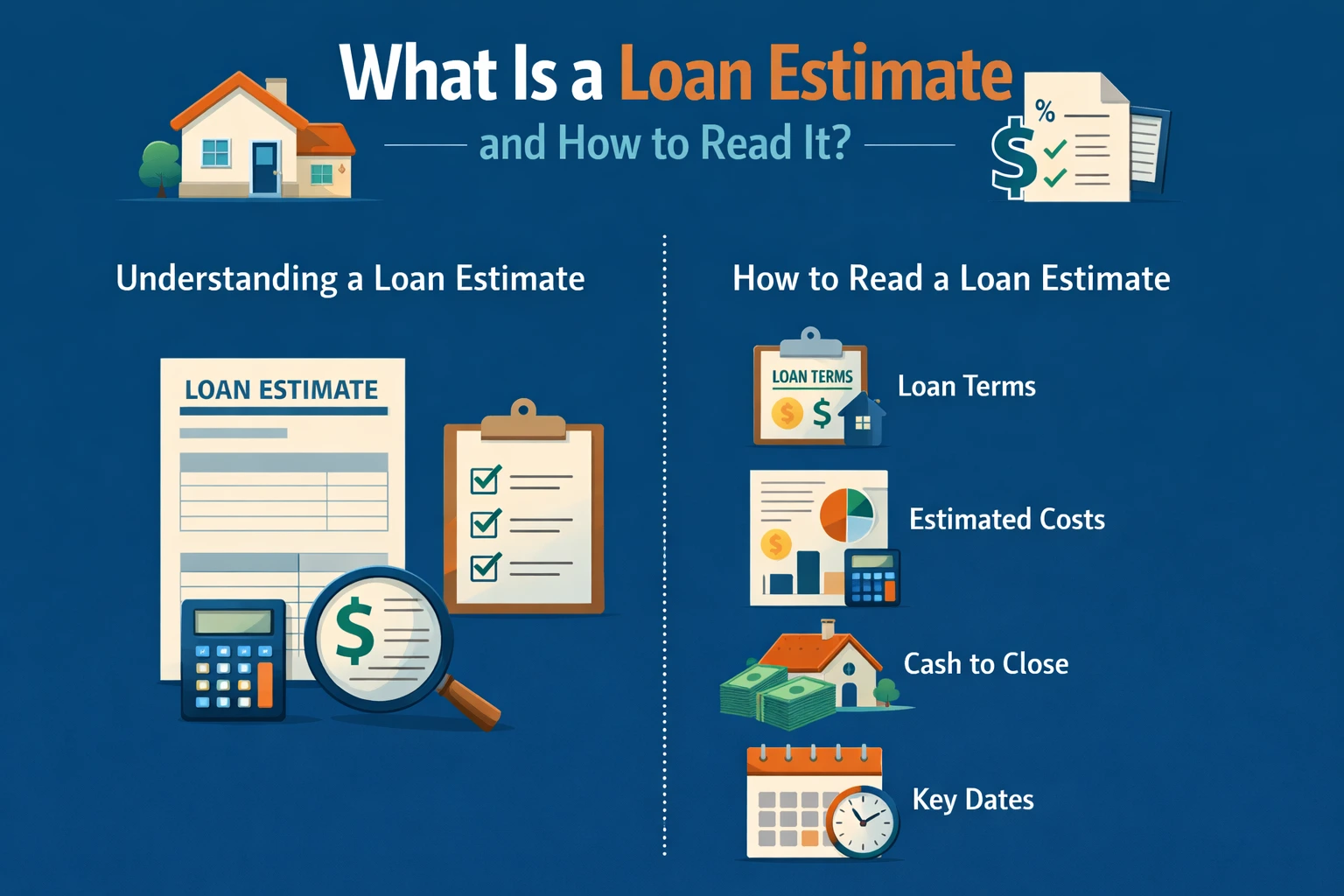

What Does a Loan Estimate Include?

A Loan Estimate is a 3-page document with key loan details.

1. Loan Terms

This section shows:

- Loan amount

- Interest rate

- Monthly principal and interest

- Prepayment penalties (if any)

2. Projected Payments

This includes your estimated monthly payment:

- Principal + Interest

- Property taxes

- Homeowners insurance

- Mortgage insurance (if applicable)

3. Closing Costs

This section outlines upfront costs, including:

- Origination fees

- Appraisal fee

- Title insurance

- Taxes and prepaid items

This helps you know how much cash you need at closing.

4. Cash to Close

This shows the total amount you need to bring to closing.

Includes:

- Down payment

- Closing costs

- Adjustments and credits

5. Loan Costs vs Other Costs

- Loan Costs → Fees charged by the lender

- Other Costs → Third-party fees (insurance, taxes, etc.)

How to Read a Loan Estimate (Step-by-Step)

Follow these steps to understand your Loan Estimate:

Step 1: Check the Interest Rate

Look at:

- Fixed vs adjustable rate

- Rate lock status

Step 2: Review Monthly Payment

Make sure the payment fits your budget.

Step 3: Compare Closing Costs

Check total costs and compare between lenders.

Step 4: Look at Cash to Close

Ensure you have enough funds available.

Step 5: Check Loan Features

Watch for:

- Prepayment penalties

- Balloon payments

- Adjustable terms

Loan Estimate vs Closing Disclosure

These two documents are similar but used at different stages.

| Loan Estimate | Closing Disclosure |

|---|---|

| Given early in process | Given before closing |

| Estimated numbers | Final numbers |

| Used for comparison | Used for final review |

Common Mistakes to Avoid

- Not comparing multiple Loan Estimates

- Ignoring small fees (they add up)

- Focusing only on interest rate

- Not checking loan terms carefully

Ready to Choose the Right Mortgage?

Understanding your Loan Estimate helps you make smarter decisions.

✔ Get a Personalized Loan Estimate

✔ Start Your Mortgage Application Today

Read More What Do Mortgage Underwriters Look For?

FAQs

What is a Loan Estimate in simple terms?

A Loan Estimate is a document that shows your loan terms, interest rate, and closing costs.

Is a Loan Estimate final?

No, it is an estimate. Final numbers are provided in the Closing Disclosure.

Can I negotiate a Loan Estimate?

Yes, you can compare offers and negotiate fees with lenders.

How many Loan Estimates should I get?

It’s recommended to get at least 2–3 estimates from different lenders.

Does a Loan Estimate mean I’m approved?

No, it does not guarantee loan approval.