Most bank statement loans take anywhere from a few days to several weeks to get approved, depending on your financial documents, lender requirements, and property details.

If you’re self-employed and planning to buy a home or investment property, understanding the bank statement loan approval timeline can help you prepare for the mortgage process in 2026.

What Is a Bank Statement Loan?

A bank statement loan is a non-QM mortgage designed for borrowers who may not qualify using traditional income documents.

Instead of tax returns, lenders review:

- Personal bank statements

- Business bank statements

- Deposit history

- Cash flow consistency

These loans are commonly used by:

- Self-employed borrowers

- Business owners

- Freelancers

- Real estate investors

Average Bank Statement Loan Approval Timeline in 2026

The timeline varies by lender, but most approvals follow this process:

| Stage | Estimated Time |

|---|---|

| Initial Application | 1–2 Days |

| Document Review | Several Days |

| Underwriting | 1–2 Weeks |

| Final Approval & Closing | Additional Days |

Overall timeline depends on how quickly documents are submitted and reviewed.

What Affects Bank Statement Loan Approval Time?

1. Document Preparation

Incomplete documents are one of the biggest causes of delays.

Most lenders require:

- 12–24 months of bank statements

- ID verification

- Asset documentation

- Business information

2. Loan Complexity

Approval may take longer for:

- Investment properties

- Jumbo loans

- Multiple income sources

- Complex business structures

3. Property Appraisal

The appraisal process can affect overall timing.

Delays sometimes happen when:

- Market conditions are busy

- Property valuation issues arise

4. Underwriting Review

Underwriters analyze:

- Deposit consistency

- Cash flow

- Credit profile

- Debt obligations

More complex files often require additional review.

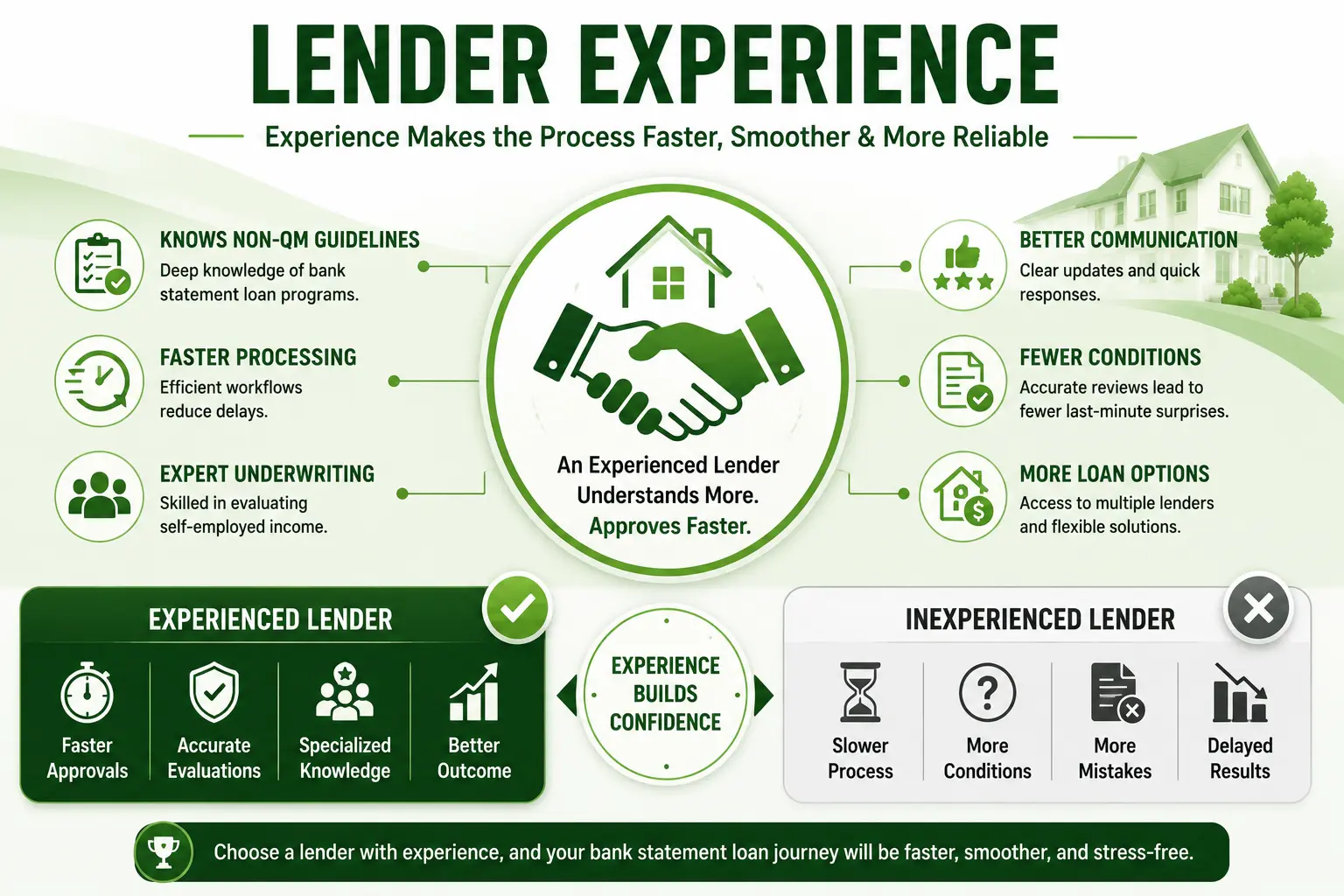

5. Lender Experience

Some lenders specialize in non-QM loans and process applications more efficiently than others.

How to Speed Up the Approval Process

Submit Documents Early

Having all bank statements and financial records ready can reduce delays.

Respond Quickly to Requests

Fast responses help underwriting move smoothly.

Maintain Organized Finances

Clear deposits and stable accounts make verification easier.

Avoid Major Financial Changes

Avoid:

- Large unexplained deposits

- New debt

- Major account changes during the process

Preparing for a mortgage application?

✔ Explore Flexible Loan Options

✔ Review Bank Statement Loan Requirements

Is a Bank Statement Loan Faster Than a Conventional Loan?

Sometimes, yes.

Because lenders focus more on bank deposits instead of extensive tax-return analysis, some borrowers experience faster approvals.

However, timelines vary depending on:

- Lender guidelines

- Property type

- Borrower profile

Example Scenario

Borrower A

- Organized documents

- Strong deposits

- Simple borrower profile

Faster approval potential

Borrower B

- Multiple businesses

- Missing documentation

- Investment property purchase

Longer underwriting timeline likely

Looking for a Simpler Mortgage Process?

Bank statement loans can provide flexible financing options for self-employed borrowers with non-traditional income documentation.

✔ Compare Your Loan Options

✔ Speak With a Mortgage Specialist

Read More Credit Score for a Bank Statement Loan in 2026?

FAQs

How long does a bank statement loan take to get approved?

Approval timelines vary, but many loans are completed within several days to a few weeks.

What delays bank statement loan approval?

Missing documents, appraisal delays, and complex financial situations can slow the process.

Can self-employed borrowers get approved faster?

Borrowers with organized financial records and strong deposits often experience smoother approvals.

Do bank statement loans require underwriting?

Yes. Lenders still review income, deposits, credit, and overall financial stability.

Is a bank statement loan easier than a conventional loan?

For self-employed borrowers, qualification can often be more flexible than traditional mortgage programs.